Avoiding shenanigans

by Doug Brodie

In this blog:

/1. Saying ‘No’

/2. Shenanigans

/3. ESG – who’s the war-monger?

/4. Jolly hockey sticks

/5. In the technical part of the income market

/6. How to gift to married children and keep it in the family

/7. Target date funds: a technical note

/1. Saying ‘No’.

(Perhaps the subtitle of this should be ‘the value of advice is not the same as the cost of an investment’).

Example 1 – The mysterious case of the £148,500 tax saving.

Back in the late 1990s a man walked off the street into our Covent Garden office at 8.30 in the morning, catching us slightly on the hop – no one ever walked in off the street, and no one has ever done since. He was the Deloitte-trained CEO of a locally based business (that you’ve heard of, that you’ve probably used); at 39 he wanted to organise his pension and his opening gambit was that he didn’t want to pay any ridiculous commissions (that wasn’t how we worked). Roll on twenty six years and that client is now 65 and has a pension pot nudging £1.8m.

His commercial life has been very up and very down over that time, mainly as CEO or CFO of FTSE 250 companies, private, listed, taken private, with core business very affected by the macro-economic trials of the last ten years. The retirement plan was always to have £x in the pension, and £y in cash from the stock awards in the company that was his employer; however, that didn’t go to plan and it’s chiefly now all pension.

Having stepped down from the sharp end and taken up a part time private equity consulting role we had an initial conversation about drawing down his tax free cash almost two years ago. We had organised ‘LTA protection’ for his SIPP back in 2014 which meant he was entitled to a pot size of £1.5m, however everything above that would be taxed at 55% when drawn. In his case, that tax would be £148,500. Then came the government’s announcement that they wanted to change the Lifetime Allowance in order to resolve the unintended consequence that meant senior medics working overtime in the pandemic were doing so for free due to perverse pension taxation.

Mr Client wanted the tax free cash – he had a mortgage to clear and interest rates were jumping up, however we had to recommend ‘no’ until we found out what the rules were going to be. We were part of HMRC’s working group on the new rules so had a good inkling of what was coming, however it was what the pension provider understood that mattered, not our views. Eventually the rules were published and we went to the client’s final salary administrator to ask for a transitional certificate, only to be told that – in their opinion – he didn’t need one. Which of course then made the client panic that instead of getting £375,000 in tax free cash (£1.5m x 25%) he would only get £268,275 (the new cap). Fortunately, the head of technical at the SIPP company was on the same working group as we were, and after much swapping of emails and letters this morning they confirmed they were happy to release the £375k, leaving the client a balance of circa £1.4m to provide income.

There’s lovely.

Example 2. Your flexible friend.

These clients are moving money into a family investment company as part of a solution for inheritance tax. We started working with them almost two years ago, interesting people to work with as he had previously been an FTSE CEO and also a director of a significant investment trust, so he knew precisely what we do, and why.

As luck had it, just as the family company was being set up they came across the house of their dreams, around the same value as their current home. Following the adage of the best laid plans, sure enough, the buyer for their home fell through in February just as they had committed to complete on the new home. And at the same time, they were committed to fund the newco. The clients needed several £X00,000s to fund the newco and wanted to raid their ISAs for the cash, knowing they would have the cash available again when their home sold.

Trouble was, their ISAs were with a mainstream firm and not ‘flexible – several years ago HMRC changed the rules to allow investors to replace any cash drawn from an ISA back into the ISA as long as it is done in the same tax year. These are known as flexible ISAs. In this client’s case we advised to not do the funding of newco till after 6th April, and in the meantime move the ISAs to a flexible provider (happens to be AJ Bell). That all being done, the cash comes from their new flexible ISAs and when the current home is sold the money can go straight back. This important – the clients are higher rate taxpayers and need the tax free income, plus by maximising the tax free income it allows them to use the ‘gifts from normal expenditure’ rules to continue giving cash away IHT free for the benefit of the grandchildren (we do expect to be on the Christmas card list of said grandchildren…). The client saves £8,000 in income tax each year on the income drawn from the money returned to the ISAs.

/2. Shenanigans

A regular reader of this newsletter told us that what he was struggling with re his retirement planning is ‘how to protect my SIPP fund from stock market shenanigans whilst providing a comfortable retirement’.

That is exactly what we want to hear from a prospective client – the objectives are clear, the anxiety is spelt out. What he is yet to learn is that this is precisely why Chancery Lane was set up by the founders, all of us over the age of 60, all bar me already retired. Having £1m in your pension and savings might make you wealthy, but it doesn’t make you financially independent without solving the income conundrum.

There’s a very gender-biased issue here: this reader, in line with many who talk to us, is creating personal anxiety and unease when he needs that least by ignoring the objective to debate the detail. It’s a thing that men tend to do, and that women tend not to do. It’s a gender trend that is demonstrated by more Haynes Manuals being bought by men than women. The objective of car ownership is to reliable, safe transportation, not an overgrown Meccano set to entertain the left side of the brain.

The answer is outlined in our research, published on our website for access to all. However, the answer is summed up in one simple diagram which we call the Key Chart for that reason:

The ‘comfortable retirement’ is the red line, the blue bars are the investment equivalent of a Weber 40 DCOE carburettor (late type).

/3. ESG – who’s the war-monger?

As Sting said, ‘I hope the Russians love their children too’, and in today’s world we have an interesting dilemma with ESG investing, Yes, we do love our children (and yours and theirs) so we would actively seek to not support those firms promoting and supporting armed conflict. That means we would want to avoid investing in Heckler & Koch, however what about Saab (warplanes), or BAE (tanks, submarines), as they respectively are market leaders in trucks and avionics? More, Rolls Royce makes jet engines for both the Typhoon warplane and also the Airbus A380. Safe to invest?

The other question that has risen to the fore is whether or not any of these arms manufacturers should be supported because they supply the items we need to protect our country, our families, as opposed to attacking others. When investors talk ESG, it’s not a binary subject.

Rolls Royce Trent 900, 84,000 lbf, diameter the same as the fuselage of a DC9.

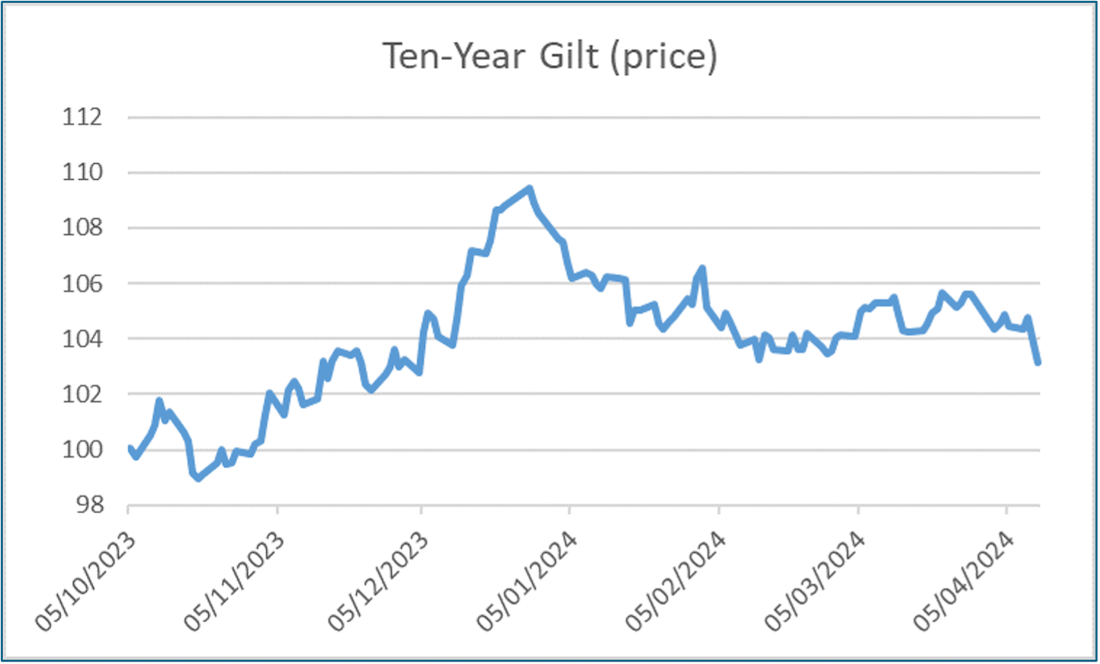

/4. Jolly hockey sticks.

Insights and data collated by Mark Glowrey and our good friends at Allia C&C.

This is the price chart for the gilt that matures in 10 years’ time – it is only risk free for the investor who holds to maturity, and that is because the government guarantees to repay at maturity at £100. If you buy it today the price is £102.40p so you are guaranteed to lose £2.40p over the next ten years – to make it a worthwhile investment you have to have calculated that the income paid each year (again, guaranteed by H.M.G.) is sufficient to make a profit.

The chart above is the capital value; the chart below is the yield (coupon income as a % of the price):

The downward curve is your hockey stick – it plots the yields that you get from buying the gilts maturing at the different years measured along the bottom X axis. You can see that in all cases the yield is above 4%, that the yields for 2 years’ time are 4.4%-ish, falling to 4.1%-ish for gilts maturing in 6 years’ time, then climbing back up to 4.6%-ish in 20 years. These are industry indicators of what the banks and giant investors are currently projecting as likely interest rate directions (not rates) in coming years.

/5. In the technical part of the income market

These are fixed term bonds issued by social housing associations – you’re unlikely to recognise any names in the table unless you happen to work in the sector. We keep an eye on the research here so that our clients don’t have to, and to check we’re covering all the relevant alternatives.

More importantly, it helps us frame our reference points – is a 5% return good? Compared to what alternative? How about 7%? Well, we know that the table above tells us that 7% is a bit on the high side for a social housing association, so that means anything else offering that rate of interest/yield should contain a similar amount or risk – ie similar likelihood of default. You can see for example, that the ‘grown up’ investment market is demanding 7.77% income from Greensleeves, even though it is ‘promising’ to repay the bond in two years’ time. If you don’t understand what you’re investing in and think yield is all, you’re likely to get sucked in by offers from companies like Home REIT.

/6. How to gift to married children and keep it in the family

Victoria Emens at RWK Goodman is a family lawyer with insightful and clear English summaries. The full outline of her note will be stored under Chancery Brain, however, this is a snapshot of the key points to consider:

Gifts

A gift of money is when the parents have no expectation that the money will be repaid and the parents will not acquire a financial interest in a property or other assets purchased with those monies.

An outright gift cannot generally be recovered by a parent in the event of their offspring’s divorce. The gift is likely to fall into the matrimonial pot for division between the parties to meet their respective needs, in the event that they separate or divorce, particularly if the funds were used to purchase the family home.

Loans

Unlike a gift, a loan is treated as a liability with an expectation or obligation that it will be repaid in the future. Such a loan will almost invariably be factored into the divorce court’s decision.

Soft loans

These are monies that are lent informally between family members or friends on good terms. They are often by verbal agreement, not documented, without a written demand for repayment and with a delay in enforcing the sum loaned.

The risk here is that the court can often determine that the soft loan is actually a gift and not a true liability or that the funds do not have to be repaid any time soon, if at all.

It will often be suggested that gifts from parents should be seen as a significant contribution to a marriage, with the argument that a gift of money should be retained by the party receiving that gift.

However, such an argument will often be overridden in lower value ‘needs’ cases, as the needs of the parties and any dependent children for housing will usually take priority.

In larger money cases, where the capital exceeds the needs of the parties, there is more scope for arguing that gifts should be retained by the party that received it.

No two cases are alike. In determining the outcome, the court is required to look at all the circumstances of each case, including the intention and expectation at the time the money was advanced.

When a parent or set of parents feel strongly that they wish to be heard when a dispute arises during a divorce over an advance, they may wish to make an application to the court to intervene in the proceedings whereupon they become joined as a party to the proceedings.

That said, the best course of action is to avoid a dispute arising in the first place, and there are various options that we can advise our clients on to help to ensure that any financial support remains in the family in the event of divorce or separation.

Early legal advice and clear and unambiguous documentation is key.

Declaration of trust

If the money being advanced is towards the purchase of a property, a deed of trust can be prepared with the property being held as 'tenants in common' with the parents being entitled to a percentage share of the property in proportion to the size of the loan.

The declaration of trust document will make it clear how much each party is to receive in the event of that relationship failing, for example, providing how the sale proceeds are to be divided when the property is later sold.

Documented loan agreement and legal charge

One option is to document any payment as a loan and, where appropriate, to also register it as a charge against a property.

This will turn it from an unsecured loan to a secured loan, but it needs to be noted that this can have implications, and often will require the lender’s agreement where there is a mortgage secured on the property.

Outright and conditional gifts

If the money provided is to be a gift, then this should be recorded in writing, making it clear it is without conditions and with no expectation that it is to be re-paid in the future. It is important that the tax implications are understood.

A conditional gift of money could be provided with it being set out in writing that the money is advanced as a gift but in the event of separation or divorce the monies will be repaid by one or both spouses.

If you’d like to speak with Victoria then please let us know: in many cases, our role is to know who the clever people are, and she has a broad experience, plus the benefit of being based in Swindon, not the expensive gilt cobbled streets of London (Ed: What, you mean like Chancery Lane?).

/7. Target date funds: a technical note

Every so often we’ll include a technical note on items that we see being pushed by marketing departments. Target date funds fall into this category – they are designed to run for a finite length of time and then mature back to cash – a bit like a gilt with a fixed date. The difference with these though is that unlike gilts there is no fixed redemption value nor a coupon. As there are ‘fixed’ elements to the funds they are often mis-sold and mis-used.

Vanguard runs ‘lifestyle’ funds and these are an example of a retail version of these funds – they have high equity percentages whilst there are many years to maturity, with the equity percentage being reduced and swapped into bonds and/or cash as the investor nears retirement. If you think about it, it’s pretty much designed to hand the investor cash at the time of retirement – pretty much designed for an investor who wants to buy an annuity – why else sell to cash at that stage?

Target date funds are actually chiefly an institutional tool, and the learned team at PMR (Portfolio Management Research) produced this summary of what the funds are, last year – this is the abstract below. Note, there are key signs here that they are not writing for retail investors like you – it states ‘reduction in portfolio risk’ which implies that it is portfolio volatility that is the risk. We have published our research elsewhere that demonstrates that volatility is a misnomer for retail investment risk – volatility is just volatility, and it is guaranteed in equity markets.

Target Date Funds (TDFs) are portfolios with a pre-defined end date, the so-called “target date,” and the essential attribute that they reduce their allocation to stocks with the passage of time. The proposition upon which TDFs are both sold and bought is that investors benefit from the consistent reduction in portfolio risk as investors progress toward the end of their applicable investment time horizon.

The manufacturers of TDFs have a clear and unambiguous motivation to develop an appealing story and associated product that encapsulates said story, so as to grow their assets under management. The pension plan sponsor’s motivation is to provide investment options that protect it from regulatory and litigation risk. Unfortunately, the data offer a different reality. The data support the conclusion that investors are harmed by the use of TDFs when sufficient time diversification is present, resulting from a sufficient number of relatively equal-sized contributions and/or withdrawals evenly dispersed over time.

Specifically, the analysis shows that: 1) the use of precious metals remains unattractive for investment time periods of 12.5 years and longer, 2) optimal starting allocations of 100% stocks remain preferable for investment time periods of 5 years and longer, and 3) the use of TDFs remains significantly harmful to investors’ wellbeing for periods of 15 years and longer.

The causality driving these results is both simple and straightforward. First, bonds and precious metals impose a severe return penalty on the investor. The geometric mean returns are −72% and −87% proportionately lower than for stocks, respectively. Second, bonds and precious metals impose extended (many decade-long) episodic eras of negative returns, unlike stocks. Third, time diversification applicable to circumstances where contributions and/or withdrawals of relatively equal size occur over extended time periods and with high frequency make the use of bonds, precious metals, and TDFs purely redundant and non-contributive.

We’ve included this research to demonstrate a couple of key points to our readers:

1) there’s a lot of background research, reading, calculation and due diligence behind our client recommendations, and

2) there is clearly a significant difference between the needs of a person’s pension portfolio and the strategy for a pension scheme with many beneficiaries, many ages, many cashflows.