When the sun rises on the first day of your retirement,

what you need is a reliable monthly income.

Get our rather marvellous Saturday morning email

A weekly email and exclusive content for people just like you

(and absolutely no boring stuff)

By submitting this form you consent to our Privacy Policy. (We’re a decent lot and promise to treat your details with respect.)

Free Income Planning Calculators

As featured in:

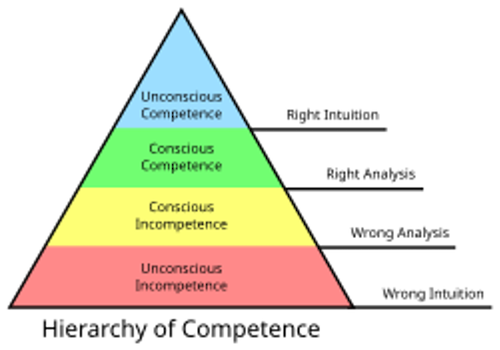

Planning with confidence

Are you ready?

Get your personal

score and report, now.

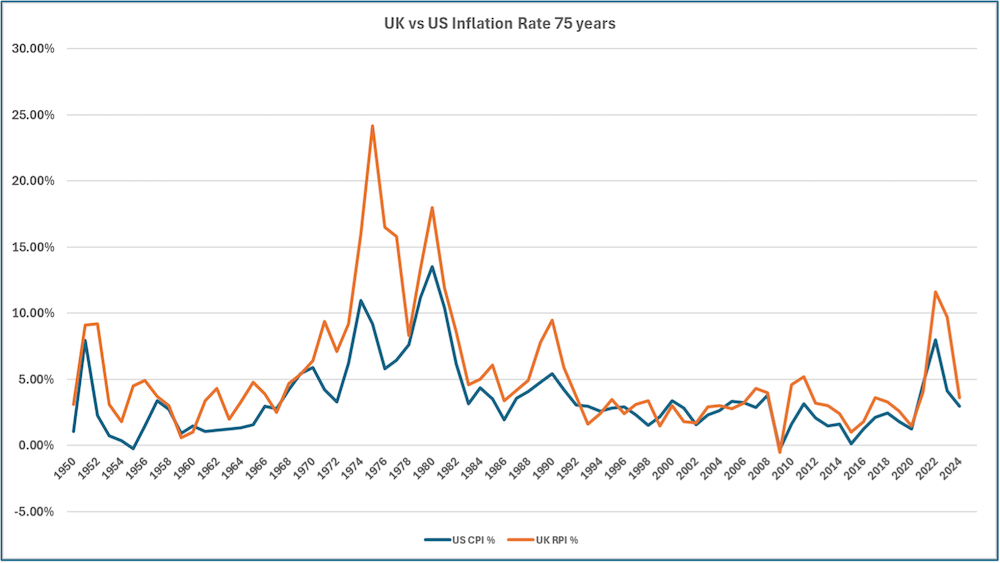

Beating inflation

Read more, or go straight to try

our RPI-analysis tools

Meet the team

The people behind Chancery Lane,

our expertise, our history.

We’re people like you

Bridget McIntyre

William Todd

Kim Lerche-Thomsen

Ian Manning

Only Chancery Lane specialises in just one thing — investing for income for baby boomers.

Bucket List Top 50

How many have you ticked off?

Wellbeing

Dealing with a new life without a daily schedule.

My Generation

What it means to be a boomer — how many of these experiences defined your life?